5 Accounts You Need By Age 20, If You Want To Be Wealthy...

All Canadians should have these 5 accounts open by age 20.

I get it, money is scary. But if you don’t learn to control it, you will never be able to obtain financial freedom or any wealth. So let’s start with the basics.

Today, I’ll break down the 5 basic accounts that ALL Canadians above 20 years old should have open.

This is another Monday edition of Matt’s Money Manifesto!

We’ll cover:

What they are

How to use them efficiently to grow your money

Where to open them

1. Checking Account

We all know what a checking account is, so I won’t waste your time with this one. A checking account should be used for 3 things, and 3 things only.

a place where your paycheck gets sent to

some day-to-day expenses (personally I use a credit card for points though)

to move money to other accounts

That’s it. It’s a checking account. No money should be saved or stored in here that is NOT going to be spent in the next few days/weeks.

2. High Interest/Yield Savings Account

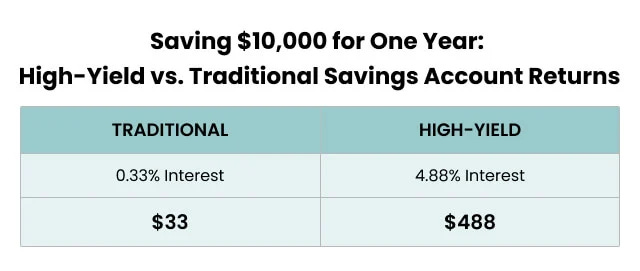

You may have heard of the standard “Savings Account”, so how is this any different? Well, as it says in the name, a “High Interest” savings account provides a HIGHER interest rate than a standard savings account.

At the time of this article, high-interest savings accounts are earning anywhere from 4% - 6% interest. Compared to a normal savings account at TD Bank, which offers 0.1%, and 1.5%, that’s a MASSIVE difference. So move that money into a better savings account!

You can find a list of all of the best high-interest savings accounts in Canada here

I personally use Tangerine’s which gives me 6% interest until the end of February

This is literally FREE money… so why the **** aren’t you doing it?

3. Tax-Free Savings Account (TFSA)

The tax-free savings account is, in my opinion, the holy grail of building wealth for Canadians. Here are a few key points:

All Canadians over the age of 18 can open a TFSA and contribute the yearly limit

(2022 = $6000, 2023 = $6500, 2024 = $7000, etc.)You invest inside of it (Stocks, Bonds, ETFs, Mutual funds, etc.)

All of the profit you make is tax-free, and you can withdraw anytime you want

It’s almost too good to be true, and that’s why they have to put a yearly limit on it.

Even if you know NOTHING about investing, please, for the love of god, just OPEN a TFSA, and start to learn the absolute basics of investing.

It will change your life

For beginners, I recommend opening a TFSA on Wealthimsple, it’s by far the most beginner-friendly platform, and they have extremely low fees, unlike the major banks!

And, to learn the basics of investing, you can check my other article, “The Basics of Stock Market Investing - A Complete Beginner's Guide”

4. First Home Savings Account (FHSA)

The FHSA was released this year (2023), and as it states in the name, it is for first-time home buyers. Some key facts:

Can only be used by Canadians who do not own a home

Can contribute $8000 a year, a maximum of $40,000

Can only withdraw for use towards the purchase of your first homer (otherwise penalties)

All withdrawals (profits on the investments) are tax FREE, and all the money that you contribute to the account can be used as a tax deduction (against your income)

Basically, it’s another great way to start saving and investing for that goal of owning your first home, which I assume all of us have. Mom’s couch can’t hold you forever, kiddo.

Open this account with whoever you want, but again, I recommend Wealthsimple or any platform of your choosing. Just avoid paying any ridiculous fees!

5. Registered Retirement Savings Plan (RRSP)

I know retirement is probably a while away for you, and that’s why this account is last. But it’s never too early to start planning for your senior life!

An RRSP is another investing account, and here are some key details

All Canadians can open an account

Can contribute a yearly limit based on your income

You can only withdraw the money when you RETIRE (there are some exceptions)

All contributions made to the account can be used as a tax deduction (against your income)

Unlike the other accounts, all gains you make on your investments are tax-deferred, instead of tax-free

This means that you will pay taxes when you withdraw the money in retirement, HOWEVER, you will be in a lower tax bracket when you retire (I assume), so therefore will pay LESS taxes on the money! Make sense?

I get it, you don’t want to think about retirement yet, but better to start early, than late. Your future spouse, kids, and yourself will thank you.

If you open all 5 of these accounts and use them PROPERLY, you are setting yourself up for financial success.

This has been another Monday edition of Matt’s Money Manifesto!

Hopefully you all enjoyed this read! Make sure to like, and drop a comment if you did :)

This was super informative as a new Canadian citizen. Thanks!